In terms of balanced growth, the US is the strongest economy in the world right now.

Here are a few charts that show the state of investment around the world. The data, taken from FRED, shows the percentage change in trailing twelve month real gross fixed capital formation from 1Q 2000 levels.

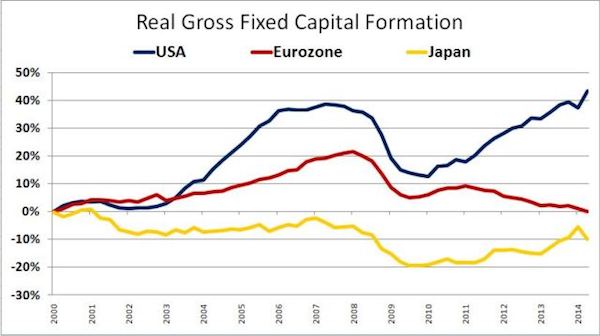

US, Europe, Japan, 1Q 2000 to 2Q 2014:

Notice the recent downtick in Japan. Is the downtick a short-term effect of the consumption tax increase, or a sign that the “Abenomics” boom is already petering out?

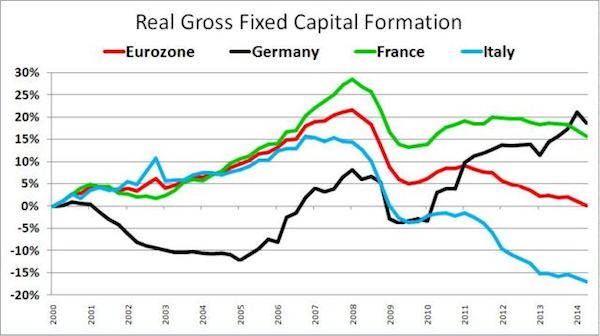

Germany, Italy, France, Eurozone, 1Q 2000 to 2Q 2014:

Notice the investment strength that Germany has seen since the crisis. This strength stands in stark contrast to the investment decline seen in the other countries. Interestingly, the situation is a mirror image of the situation of the prior decade, wherein German investment remained subdued while investment in the other countries experienced a boom.

The subdued investment in Germany, coupled to the unproductive investment boom experienced by the rest of the Eurozone, created wage, price and competitiveness differentials between the countries that now stand at the heart of the Eurozone problem. German goods and services are simply too cheap relative to the goods and services of the rest of the Eurozone for the countries to remain in a currency union that precludes exchange rate adjustment.

The boom in employment that Germany, due to its significant competitive advantages, is experiencing as it attracts consumption and investment flows from the rest of the Eurozone is the system’s attempt to rebalance in the only way that it can. The problem is that the rebalancing is extremely painful for the rest of the Eurozone countries, which are experiencing the opposite of what Germany is experiencing–depressed investment, high unemployment, and a tendency towards deflation.

The only politically viable mechanism for the system to restore balance is for Germany to “boom” more, to take on more inflation relative to the other countries, which will raise the relative prices of goods and services in Germany, and create conditions where consumption and investment flows begin to naturally move back in the other direction, towards the rest of the continent. If Mario Draghi’s monetary experiments will have any hope of saving the Eurozone, the hope will rest on that mechanism: stimulating the German economy and raising German inflation in a way that helps restore relative price competitiveness in the other countries.

Spain and Greece, 1Q 2000 to 2Q 2014:

These countries had enormous residential investment booms in the last decade, five times as large as the Eurozone in aggregate. The booms did not lead to appreciable increases in Spanish or Greek productivity, though they increased wages and prices, which is why Spain and Greece now have a competitive deficit relative to Germany–a deficit that cannot adjust via the exchange rate, because the countries are in a single currency union.

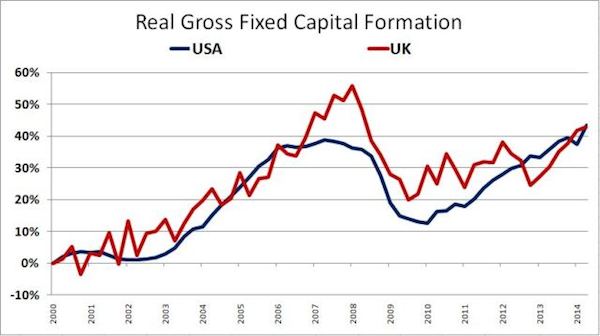

United States, United Kingdom, 1Q 2000 and 2Q 2014:

These economies tend to track each other, despite the distance between them. The UK is doing reasonably well right now, much more like the US than the rest of Europe.

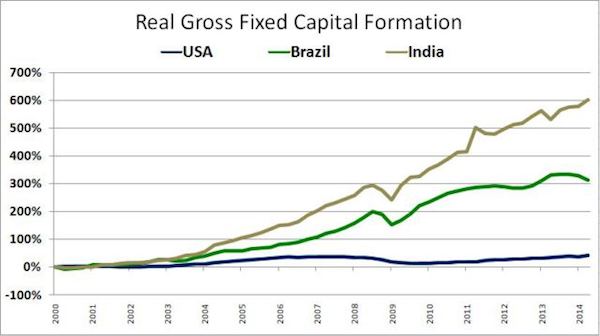

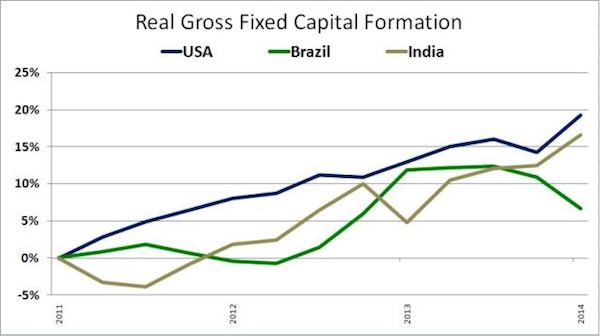

United States, Brazil, India, 1Q 2000 to 2Q 2014:

From an investment perspective, the emerging market boom of the last decade was much larger than the US housing boom. The challenge for the emerging markets going forward will be to digest the large credit expansion associated with that boom, some of which was surely unproductive. Both countries have significant inflation problems, completely different from the problems faced by the developed world.

United States, Brazil, India, 2Q 2011 to 2Q 2014:

Since 2011, investment in the US has actually been stronger than in India and Brazil. At present, Brazil is showing clear signs of being in recession.

Some thoughts:

In terms of balanced growth, the US is the strongest economy in the world right now. On a netbasis, fiscal and monetary policy in the US are not as accomodative as they should be. But they’re close enough. The combination of tight fiscal policy and extremely loose monetary policy is where the problem lies–it’s a suboptimal combination, given the circumstances.

Europe desperately needs a large, deficit-financed fiscal stimulus program to shore up the savings-investment gap in its private sector. Germany needs to lead the way on that front, aggressively stimulating its own economy so as to produce higher domestic inflation. Higher inflation in Germany will make the rest of the Eurozone more competitive and will provoke a sustainable reversal of consumption and investment flows back towards the rest of the continent. Monetary stimulus may help some at the margin, but with long-term interest rates already at record lows, with banks and households eager to deleverage, and with asset prices already elevated, particularly in the residential sector, it’s unlikely to get the job done.

Japan is at a crossroads. The consumption tax hikes were unnecessary and ill-advised. Japanese policy makers continue to show a lack of understanding of government debt. They don’t understand what the actual risks are.

To be clear, the risk that large government debt poses in Japan, and in any depressed economy, is not the risk of a bond market “revolt.” Governments fund themselves at the short-end of the curve, a part of the curve that they themselves fully control, through their central banks. A “revolt” is therefore impossible. To the contrary, the risk of large government debt is that someday, well out into the future, the economy will be in a genuine boom again. In such an environment, higher interest rates will be necessary to contain inflation. The government will then have to choose between leaving rates low or zero–a choice that could spur intolerably high inflation, asset bubbles, stagnant real economic activity given the lack of price stability, capital flight, unwanted currency depreciation, a currency crisis, or all of the above–or raising rates and dramatically increasing the interest cost on the debt, given the high degree of leverage. But if the interest cost on the debt rises substantially, the government will have to engage in aggressive austerity. Such austerity is socially divisive and economically destabilizing. And so neither choice is attractive.

But there’s no reason for Japan to forego recovery altogether, forever, simply because the government debt will be large when it is finally achieved. Japanese policymakers need to focus on getting to the destination first–a durable, self-sustaining expansion. Once they get there, then they can worry about implementing measures to deal with the large debt, as the heavily-indebted US and UK governments successfully did in the aftermath of World War II. If Japan has to enact substantial tax hikes and spending cuts at some point in the future, when the economy is overheating, then fine. The worst that will happen is that the country will end up back in a recession, which is effectively what it is trying to get out of right now. And if the country ends up experiencing a few years, or a decade, of double-digit inflation, because the tax hikes and spending cuts are too little, too late, then fine. Worse things have happened. The inflation will eat away at the debt in real terms and pull the system towards a stable equilibrium.

Brazil and India have classic inflation problems. To deal with these problems, they need to institute supply-side reforms alongside tighter monetary policy, so as to ensure that capital goes to its most efficient destinations. Brazil needs to focus more on supply-side reforms, as its monetary policy is already reasonably tight.

Photo credit: Telegraph