The Most Valuable Office in the World Right Now Might Be Ten People Who Know How to Find Power, Water, and Chips Anywhere on Earth

By Futurist Thomas Frey

A Problem That Looks Like an Opportunity

Every major infrastructure shortage in history has eventually produced a new class of specialized developer — a category of operator that doesn’t just build the thing the world needs, but builds the organizational capability to build it faster, cheaper, and more reliably than anyone else. The railroad era produced engineering firms that could survey, finance, and lay track across continents. The oil boom produced wildcatting companies that specialized in finding reserves nobody else was looking for. The telecom expansion produced tower companies that turned site acquisition and permitting into a repeatable system rather than a one-off ordeal.

We are in the early days of an equivalent moment in AI infrastructure, and the organizational model that will define it has not yet been fully invented. The demand for compute is doubling roughly every two years. The constraints on where and how you can build the facilities to supply that compute are multiplying just as fast. What the market desperately needs — and what does not yet exist in coherent form — is a venture studio purpose-built to solve the data center problem at speed and at scale.

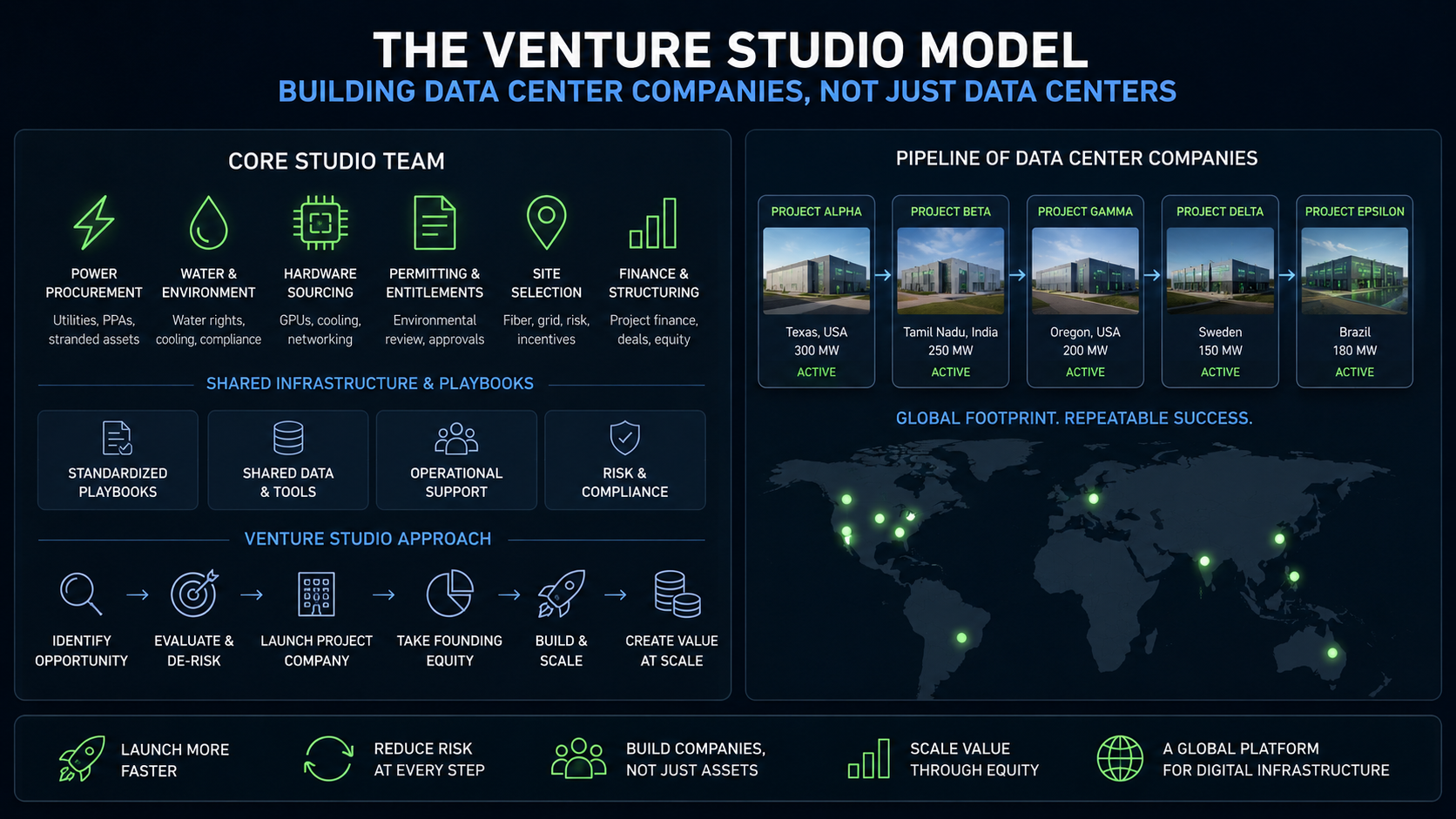

Not a real estate developer. Not a venture capital firm. Not a hyperscale operator. Something newer and more operationally specific: a small, expert team operating out of a single office, with deep specialized knowledge in power procurement, water rights, chip sourcing, permitting, and global site selection — that systematically finds the locations, assembles the resources, and launches the facilities the AI economy cannot function without.

What a Venture Studio Actually Does

The venture studio model is worth distinguishing from venture capital because the difference matters here. A venture capital firm writes checks into other people’s companies and hopes for returns. A venture studio co-founds companies, provides shared operational infrastructure, contributes domain expertise as a co-builder, and retains equity in what it creates. Studios like Idealab, Atomic, and Human Ventures have demonstrated that when you concentrate a specific set of capabilities in a shared operational environment and apply them repeatedly to related problems, you produce outcomes that neither a solo founder nor a traditional investor can match.

Applied to data center development, the studio model looks like this: a core team of perhaps eight to twelve people, each a world-class specialist in one of the five or six variables that determine whether a data center project succeeds or fails. A power procurement expert who understands how to negotiate with utilities, identify stranded energy assets, and structure power purchase agreements in jurisdictions from Texas to Tamil Nadu. A water rights attorney and hydrologist who can evaluate cooling feasibility and regulatory exposure in any geography. A chip and hardware sourcing specialist with the relationships to secure GPU allocations, cooling hardware, and networking equipment in a market where lead times are measured in years. A permitting and entitlement expert who knows how environmental review processes actually work in a dozen countries. A site selection analyst who thinks in terms of fiber routes, seismic risk, political stability, tax incentive structures, and grid interconnection queues simultaneously.

This team does not build one data center. It builds the capability to evaluate, launch, and capitalize dozens — spinning up individual project companies, taking founding equity in each, and applying the same specialized playbook to a new location every few months.

Does This Already Exist?

The honest answer is: not really, and not yet — though pieces of it are beginning to appear.

There are infrastructure-focused investment firms, notably Generate Capital and Brookfield Renewable, that understand the capital side of large energy and compute projects. There are hyperscale developers — Equinix, Digital Realty, Iron Mountain — with deep operational expertise, but they are large enterprises optimizing existing portfolios, not studios spinning up novel projects. There are a handful of emerging AI infrastructure funds, including one backed by former Google and Microsoft infrastructure executives, that are moving in this direction philosophically.

But a true venture studio — small, focused, founder-minded, equity-retaining, and organized specifically around the repeatable capability of launching data center projects in non-obvious locations — does not exist as a coherent, named category. The closest analogies are in the energy sector, where companies like X-Caliber Capital and certain family offices have quietly built site-acquisition and permitting expertise that they deploy across multiple projects. But even these are primarily capital vehicles rather than operational studios.

The gap is real, the timing is urgent, and the economics are extraordinary.

Why Non-Obvious Locations Are the Entire Game

The conventional data center geography — Northern Virginia, the Pacific Northwest, Dublin, Singapore, Phoenix — is exhausted. Interconnection queues in these markets now stretch four to seven years. Land costs have escalated dramatically. Local resistance is intensifying. The tax incentive structures that once made these locations attractive have been renegotiated or eliminated as communities have recognized the leverage they hold.

The next decade of data center development will be won by whoever can find and develop the locations that everyone else overlooked — and the expertise required to do that is genuinely rare and not easily assembled.

Consider what non-obvious looks like in practice. Stranded natural gas fields in the Permian Basin, where flared gas that would otherwise be burned off can be captured to generate on-site power for co-located compute facilities — eliminating both the fuel cost and the transmission dependency in a single stroke. Former industrial sites in the American Midwest with existing heavy electrical infrastructure, access to freshwater from the Great Lakes watershed, and land costs a fraction of coastal markets. Geothermal regions in Iceland, Kenya, and the Philippines where 24/7 renewable power is available at costs that no solar or wind project can match and where cooling benefits from ambient temperatures. Hydroelectric surplus corridors in Canada, Norway, and Paraguay where power is abundant, cheap, and clean. Special economic zones in emerging markets where governments are actively competing for the tax base and employment multiplier that data center campuses bring.

Each of these locations requires a completely different expertise stack to evaluate and develop. The stranded gas play requires understanding of flaring regulations, pipeline infrastructure, and gas processing economics. The Icelandic geothermal play requires navigating a small country’s land use and energy regulatory environment in Icelandic. The Midwest industrial site requires environmental remediation assessment and utility interconnection negotiation with a mid-size regional provider. No single hyperscale operator has the organizational agility to pursue all of these simultaneously. A venture studio structured around portable expertise rather than fixed infrastructure can.

The Team That Wins This Decade

The founding insight of a data center venture studio is that the constraint on AI infrastructure is not capital. There is extraordinary capital available for compute infrastructure — sovereign wealth funds, hyperscale operators, infrastructure REITs, and private equity are all chasing viable projects. The constraint is viable projects. The constraint is the specialized human knowledge required to find the power, secure the water, procure the hardware, navigate the permitting, and assemble the pieces into something a capital partner can fund and a customer can contract.

A ten-person studio that can reliably produce viable, fully diligenced, permit-ready data center projects in locations with secured power and water is not just a business. It is a critical infrastructure company operating at the most important bottleneck in the global economy.

The tough questions are worth asking directly. Does the studio model generate the kind of returns that attract the talent required? The answer depends entirely on equity structure — a studio that retains ten to fifteen percent founding equity in each project company it launches, across a portfolio of twenty projects over five years, could represent extraordinary value creation if the underlying projects succeed. Can a small team actually move fast enough to matter, given the multi-year timelines of infrastructure development? The answer is that speed in this context means starting the right projects two years earlier than a conventional developer would — which, given current demand trajectories, is the difference between being ahead of the market and being irrelevant to it.

The window for building this studio is open right now. The demand is compounding, the locations are available, and the organizational model has not yet been claimed.

The most valuable real estate in the world right now might be ten desks in a single office occupied by the right ten people.

Related Articles

Facilities Dive — Small, Connected Data Centers Will Power AI, a Builder Says https://www.facilitiesdive.com/news/small-connected-data-centers-will-power-ai-a-builder-says/818162

The Washington Post — Silicon Valley Is Building a Shadow Power Grid for Data Centers Across the U.S. https://www.washingtonpost.com/business/2026/02/19/data-centers-power-grid-ai

Bloomberg — The Race to Build AI Infrastructure Is Creating a New Class of Developer https://www.bloomberg.com/news/articles/2025/ai-infrastructure-data-center-developer-venture