A column on the quiet death of automobile culture and the mobility revolution already underway

Here is a question worth sitting with: what if the single most transformative shift in transportation history happened without a press release, without a ribbon-cutting ceremony, and without most of us noticing?

That is exactly what occurred. The global market for internal combustion passenger vehicles quietly peaked in 2017 — and according to the International Energy Agency, has since fallen by 30%. The car as the centerpiece of modern civilization is beginning a long, slow exit. We have arrived at Peak Car.

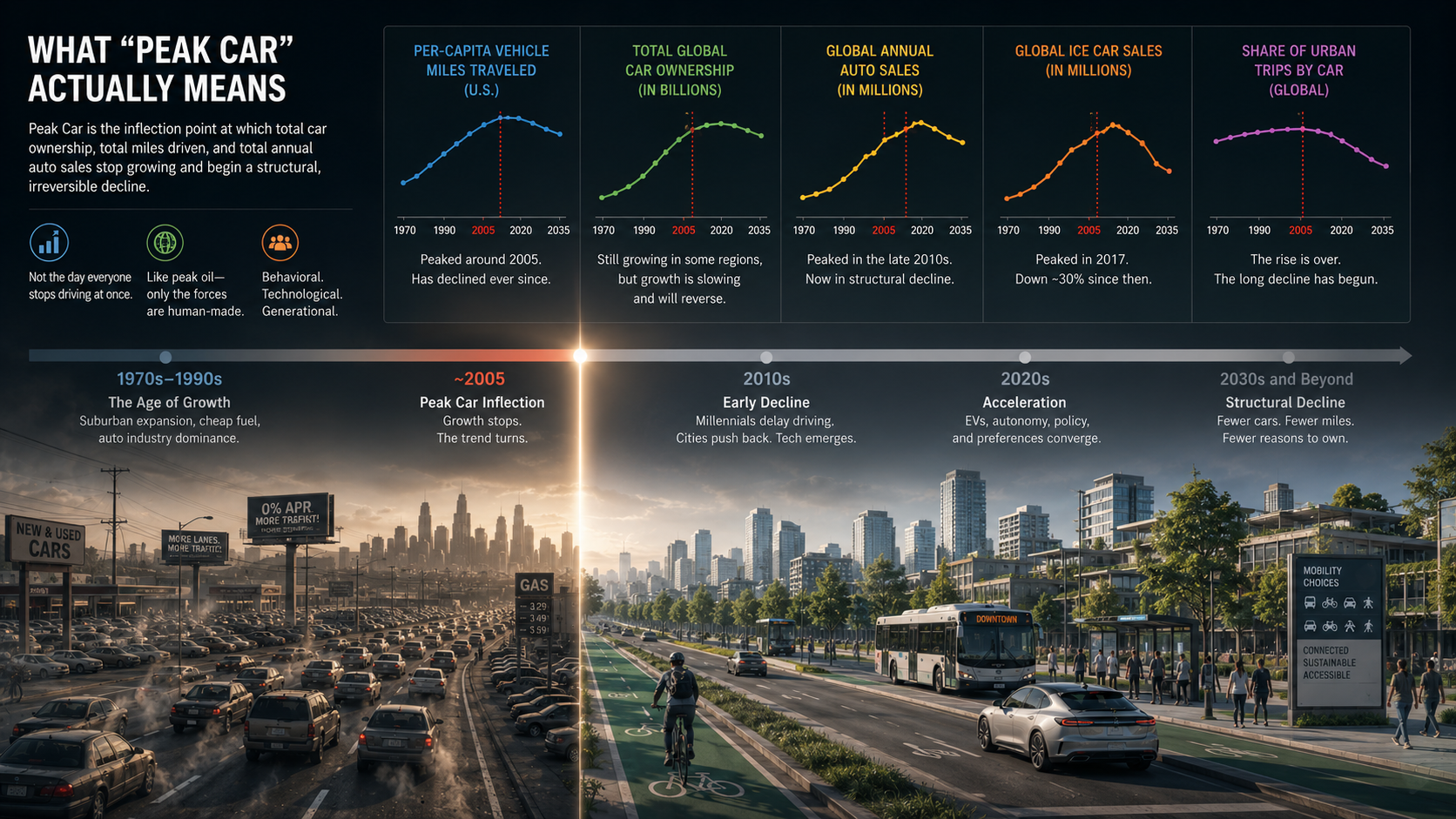

What “Peak Car” Actually Means

Peak Car is not the day everyone stops driving at once. It is the inflection point at which total car ownership, total miles driven, and total annual auto sales stop growing and begin a structural, irreversible decline.

Think of it like peak oil — the concept that global oil production would eventually hit a ceiling before declining permanently. Peak Car works the same way, only the forces driving it are not geological. They are behavioral, technological, and generational.

The United States actually hit this threshold earlier than most realized — around 2005 for per-capita vehicle miles traveled. Europe followed. Now the contagion is spreading globally, even as developing markets in Asia and Africa still show growth. Global sales of pure internal combustion engine cars peaked in 2017 and have since fallen by 30%, a data point the auto industry would prefer you not dwell on too long.

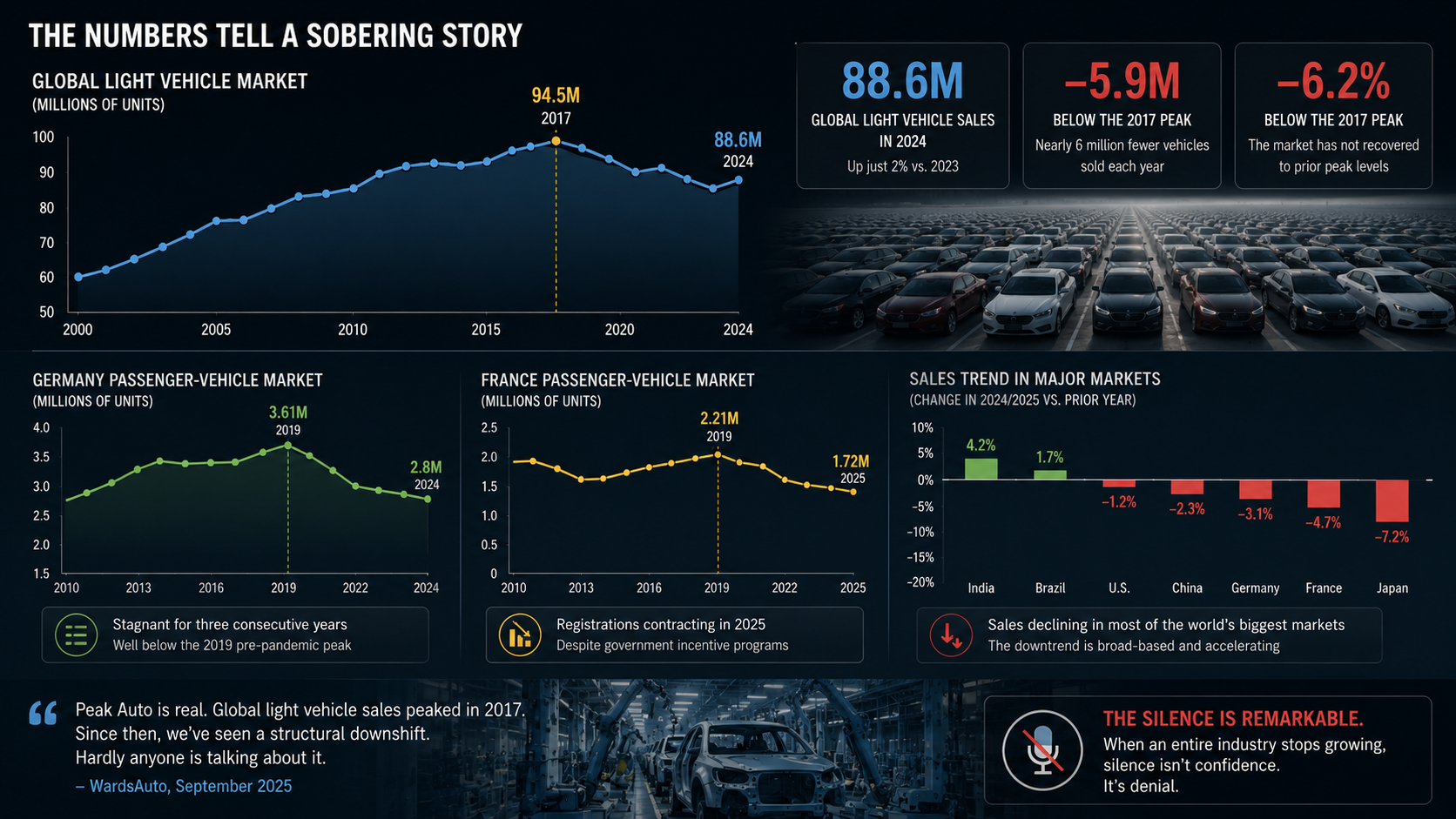

The Numbers Tell a Sobering Story

The evidence is no longer speculative. It is in the sales reports, the production data, and the boardroom projections of every major automaker on earth.

The last peak for the global light vehicle market hit 94.5 million units in 2017. In 2024, the market registered unspectacular growth of just 2%, landing at around 88.6 million units — still nearly 6 million vehicles per year below that prior peak.

Meanwhile, Germany’s passenger-vehicle market remains largely stagnant, with sales near 2.8 million units for three consecutive years — well below the 2019 pre-pandemic peak of 3.61 million units. France told a similar story in 2025, with registrations contracting despite government incentive programs. Sales in most of the world’s biggest markets have begun to decline, meaning the industry may have reached Peak Auto — a conclusion that WardsAuto reached in a September 2025 analysis with the candid observation that “hardly anyone is talking about it.”

That silence itself is remarkable.

From “Just-in-Case” to “Just-in-Time”

For over a century, the automobile represented something profound — freedom, identity, status, independence. People bought cars just-in-case they needed to go somewhere. The car sat in the driveway 22 hours a day, slowly losing value, accumulating insurance premiums, and requiring maintenance, just so it would be there when needed.

Consider what that actually costs. Finance charges, licensing, taxes, insurance, fuel, oil changes, registration renewals, parking fees, and the psychological overhead of complying with thousands of laws — speed limits, stop signs, parking restrictions, emissions checks — all layered on top of each other, year after year.

The ownership model has been quietly reframed. Today’s younger generation increasingly asks a different question: why own the whole car when you can simply summon a ride? Why carry the asset when you can access the utility?

This is the shift from just-in-case to just-in-time — and it is not a fringe philosophy. It is showing up in the data, in falling license rates among 20-somethings, and in the surging demand for services that deliver mobility without ownership.

The Robotaxi Is No Longer a Thought Experiment

When the original Peak Car thesis was written in 2015, autonomous vehicles were mostly a Silicon Valley promise. Today they are a business reality, albeit an early one.

Waymo’s fleet grew from approximately 1,500 robotaxis in May 2025 to roughly 2,500 by November, and the company now completes more than 250,000 paid rides per week. It has expanded beyond San Francisco and Phoenix into Miami, Detroit, Baltimore, Philadelphia, and a growing roster of U.S. cities. Waymo reached 100 million fully autonomous miles driven on public roads in July 2025.

The numbers behind this market are staggering. The global robotaxi market was estimated at nearly $2 billion in 2024 and is projected to reach $43.76 billion by 2030, growing at a compound annual rate of over 73%.

To put that in human terms: within this decade, pulling out your phone and summoning a driverless vehicle will be as mundane as ordering a pizza. The car that costs you $800 a month in payments and sits idle in a parking garage while you work will seem, in retrospect, like a peculiar and expensive habit.

A New Business Model Emerges from the Wreckage

The legacy auto industry faces a structural paradox. Its entire business model is optimized for selling as many individual vehicles as possible. But the world it is selling into is restructuring around fleets, not households.

Fleet operators buying 10,000 vehicles at a time are fundamentally different consumers than families buying one vehicle every five years. They care about total cost per mile, reliability records, and maintenance intervals — not cup holders or sound systems.

This will push automakers toward building fewer, more durable vehicles designed to run a million miles rather than 150,000. Margins will come from mobility services and per-mile licensing, not sticker prices.

The collateral damage will be extensive. Insurance companies lose as autonomous vehicles eliminate most accidents. Auto finance companies lose as individual ownership declines. Dealerships, already under pressure from direct-to-consumer manufacturers, face an existential reckoning. Traffic courts, parking structures, and the entire ecosystem of human-error-dependent automotive infrastructure will begin a slow-motion dissolution.

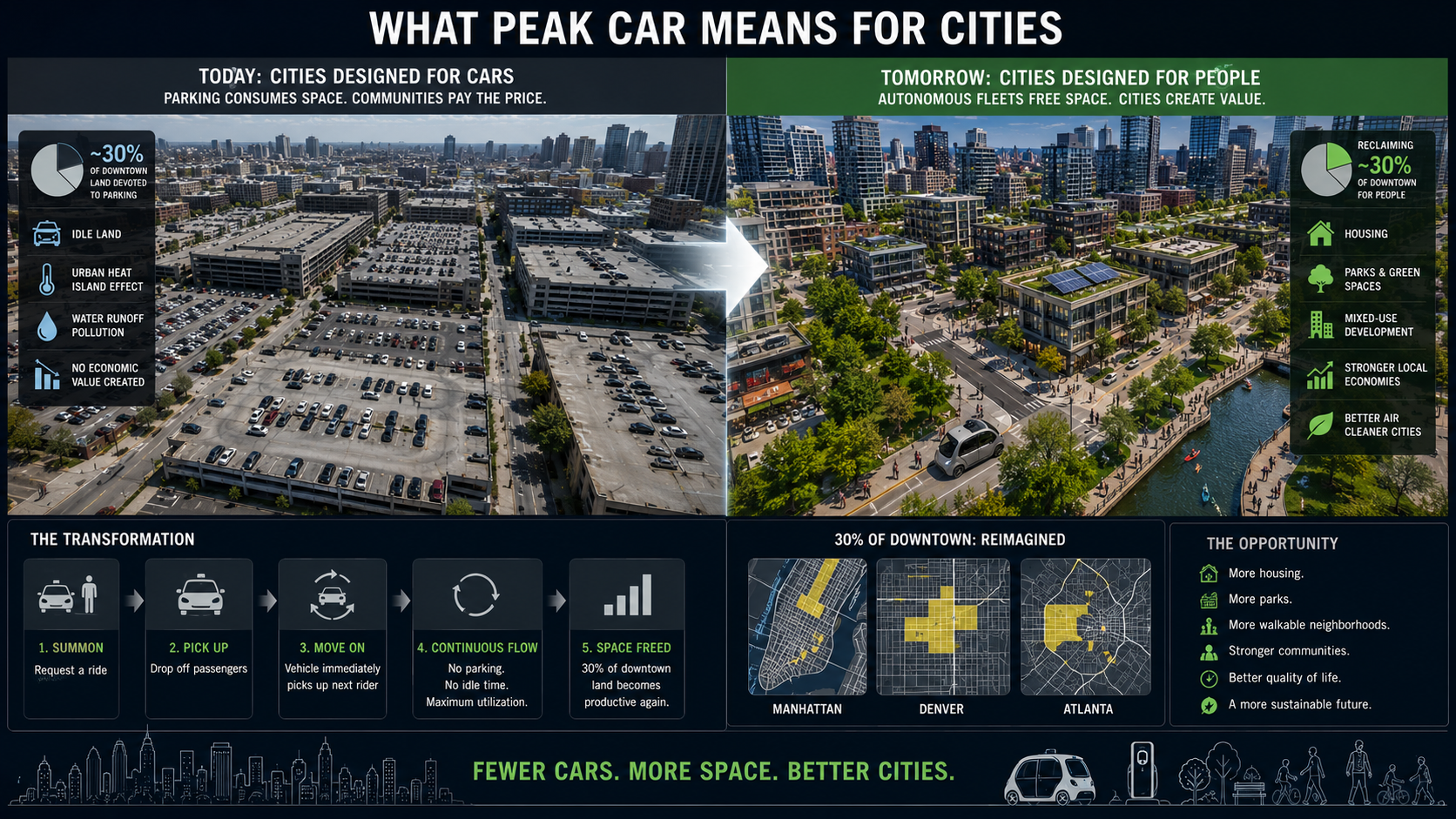

What Peak Car Means for Cities

This transition is not just good for consumers. It is potentially revolutionary for urban planning.

Today, an estimated 30% of land in the average American downtown is devoted to parking. That is prime urban real estate sitting idle, baking under the sun, generating nothing except heat and water runoff. As autonomous fleet vehicles drop passengers and immediately pick up the next one — circling continuously rather than parking — the demand for that space collapses.

What do you do with 30% of downtown Manhattan, downtown Denver, or downtown Atlanta when parking garages become obsolete? You build housing. You build parks. You build mixed-use neighborhoods that are actually walkable.

City planners who understand what is coming are already thinking about this. The ones who don’t will be caught flat-footed, approving parking structures that will be repurposed within a decade.

The Path Will Not Be Smooth

None of this will unfold without turbulence. Autonomous systems will fail in ways that dominate headlines. Regulators will move unevenly — California and Arizona lead while other states drag. Labor disruptions will be significant as millions of driving jobs slowly disappear. Cybersecurity vulnerabilities in connected vehicle systems represent a serious and underappreciated threat.

The transition also will not be uniform across the globe. Africa, with its high birth rates and underdeveloped infrastructure, is nowhere near Peak Car. India is still decades away. The global headline number will mask significant regional divergence.

But the direction of travel is no longer in doubt. The forces converging — declining ownership among younger generations, the economics of autonomous fleets, the failure of cities to absorb more cars, and the maturation of on-demand mobility — are structural, not cyclical.

The Bigger Picture

Peak Car is not a story about the decline of an industry. It is a story about the restructuring of how human beings move through the world — and what they do with the time and money they reclaim in the process.

The average American driver spends nearly an hour a day behind the wheel. Multiply that by the 144 million Americans who commute, and you are looking at an extraordinary amount of human attention that could be redirected toward productivity, learning, rest, or connection.

The car was a remarkable tool. For a century, it gave people freedom that prior generations could not have imagined. But every transformative tool eventually gives way to something better.

We are not at the end of mobility. We are at the beginning of something far more interesting.

Related Articles

WardsAuto — Peak Auto: Why the Global Auto Industry Has Stopped Growing https://www.wardsauto.com/news/peak-auto-why-the-global-auto-industry-has-stopped-growing/799098/

International Energy Agency — What Next for the Global Car Industry https://www.iea.org/reports/what-next-for-the-global-car-industry/executive-summary

S&P Global Mobility — Autonomous Ride-Hailing Grows in Key U.S. Markets https://www.spglobal.com/automotive-insights/en/blogs/2025/12/autonomous-ride-hailing-grows-key-us-markets

Just Auto — Global Automotive Market Forecasts for 2025 https://www.just-auto.com/features/global-automotive-market-forecasts-for-2025/

ResearchAndMarkets / BusinessWire — Robotaxi Market Size, Share & Trends Analysis Report 2025–2030 https://www.businesswire.com/news/home/20250805344168/en/Robotaxi-Market-Size-Share-Trends-Analysis-Report-2025-2030