The Fed is warning of several risks to the economic recovery process including damaged labor market dynamics and the potential for a long and deep recession.

Don’t underestimate COVID-19 and the global scale of the economic crisis.

We see the risks for stocks as tilted to the downside and expect a correction lower driven by a rotation out of the mega-cap tech leaders.

The FOMC met this week for its first Fed funds interest rate decision since the two emergency cuts in March. As expected, the policy rate was left unchanged at 0% with the markets focusing more on the various relief measures in response to the coronavirus pandemic and now looking ahead towards the economic rebound.

Indeed, judging by the market action over the past month, financial conditions have at least stabilized with asset prices rallying significantly from the lows in March. That being said, the policy statement included some of the darkest languages you’ll ever see from a central bank citing the coronavirus outbreak as causing “tremendous human and economic hardship and inducing sharp declines in economic activity and a surge in job losses.” Comments made during the press conference by Chairman Powell made it clear that the Fed expects a long road to recovery with considerable risks. We argue that this outlook is deeply bearish for stocks with risks tilted to the downside.

This Won’t Be a V-Shaped Recovery

There was an interesting exchange during the press conference with Powell responding to questions from Heather Long with the Washington Post. The reporter pointed to a comment in the Fed statement mentioning “medium-term risks to the pandemic”, noting that it sounds like the Fed expects a long recovery.

Powell explained that the medium-term here refers to the “next year or so” and added some color to the risks it sees to the outlook over this period. The response to this question from the video replay begins at the 16-minute mark. To summarize, the Fed sees the following challenges and risks to the outlook including:

- Uncertainty over the pandemic.

- The risk of deep and longer-lasting unemployment.

- The potential for a wave of defaults among small- and medium-sized businesses.

- The global aspect of the crisis and its impact on the U.S. economy.

Don’t Underestimate COVID-19

We think the comments here are important as it may have poured some cold water on the broader enthusiasm financial markets have been exhibiting in recent weeks. In our view, Powell and the Fed do not expect a “V-shaped” recovery and see longer-lasting disruptions to economic activity through 2021 as the base case.

We’ll break down each part of Powell’s response based on our transcription.

First it’s the virus, how long will it take to get it under control, will there be additional outbreaks, will there be drugs that can treat it or vaccine of some kind? All of that is shrouded in uncertainty.

Our take here is that the market has underestimated COVID-19 since the earliest headlines back in January and the outbreak in China which continues to defy expectations. In February, White House economic advisor Larry Kudlow famously said the virus was “contained” and pretty close to “airtight”. That turned out to not be the case.

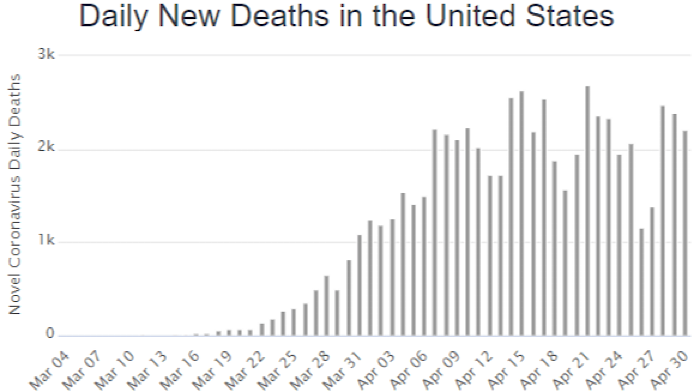

In early April, markets rallied as the estimates for cumulative deaths in the U.S. through August were revised down to around 60k from a prior 100k to 200k based on the leading IHME model, regarded as evidence that social distancing measures were working.

Unfortunately, through April the U.S. death toll has already reached the 64k figure with the original target of 100k likely back on track. Even as data shows new cases are slowing consistent with guidelines to begin reopening the economy, the concern here is that relaxing restrictions may reignite a new outbreak. The official death toll continues to be alarming with 2,201 on April 30th.

(Source: Worldometers.info)

The big headline this week was some positive trial data from Gilead Sciences’ (NASDAQ:GILD) remdesivir as a treatment for COVID-19 patients that may be able to shorten recovery time in seriously ill patients. It was also reported that the FDA is set to allow an emergency use exemption for the drug.

While we’re all hoping for the best outcome here, keep in mind that it’s still unclear how effective the treatment is. We argue that even it turns out remdesivir can indeed save lives and reduce the mortalities by a certain percentage, it does not eliminate the risk or solve the public health crisis.

Beyond remdesivir, a combination of other drugs that can reduce deaths by any amount would be a breakthrough. Still, we argue this may not be enough to restore consumer spending behaviors which is crucial for maximum productivity. The result is that the longer the disruptions last, the more pressure it adds to economic activity and financial conditions. Regardless of how the next couple of months play out, we believe the damage has already been done and will last even after the virus has been contained.

Structural Unemployment

The next risk that Powell brings up is labor market dynamics. While he avoided estimating a peak unemployment rate, it’s likely to head into the double digits during Q2. From the press conference:

The second issue and this is a very substantial one, is the possibility of damage to the productive capacity of the economy through a couple of channels. The first is just workers who may be unemployed for an extended period and that person can lose the skill that are needed and lose touch with the labor force and have trouble restarting their careers. That’s a feature of a deep and long recession and that’s something we gotta watch out for.

Powell points to the potential damage to the “productive capacity of the economy”. What Powell is referring to here is the risk of structural unemployment, which is based on companies reorganizing following a major change. This is more serious than just temporary layoffs as it can keep out many workers who previously had jobs but are no longer needed once businesses are adapted to the new realities in a post-COVID-19 world.

The understanding is that many furloughed workers in service industry jobs like restaurants and hospitality will eventually be brought back when those businesses can reopen. The risk, however, is that not all those jobs will come back, and people will be unemployed for longer. Jobs in other industries are at risk too.

A business may find they need to reopen with fewer employees to remain profitable. Companies will also face uncertainties related to trends in demand and be hesitant to add new hires or expand operations. A negative feedback loop in the economy between unemployment, consumer spending, investment sentiment can spread to various sectors. Unemployed or under-employed people simply have less discretionary spending power which ultimately leads to lower corporate revenues, earnings, and investment capacity in the economy. This is bearish for all companies.

The other problem that can pressure long-term unemployment is the threat of small- and medium-sized businesses closing permanently. Much of the efforts of the relief efforts right now on the fiscal side are based on liquidity or loans for payroll protection. It also came up in the press conference that these measures may not reach the companies most in need as they may not be able to repay the loans or have larger liabilities. The Fed sees the potential for a wave of defaults as a real possibility. From Powell’s comments:

The third is just businesses. Thousands of great small and medium-sized businesses all over the country and they are worth so much more to the economy than just the sum of their net assets. They’re job creators and really important. If we see a wave of insolvencies that could be damaging to the economy over time. The good news is that we have policies that can address those things, but not perfectly, so that’s another risk.

The key phrase for us in this quote is “not perfectly” in regards to policies that can be used to address the stress environment. This means that the Fed expects there to be leakages or companies falling through the cracks. Again, going back to our original point, the consequences here appear to go beyond just the public health crisis and will linger through 2021.

This is a global crisis

We sense that some investors are losing track of the bigger macro picture. The reality here is that the economic collapse is just as bad or worse in most other regions of the world that have resorted to the same lockdown measures in their effort to stop the coronavirus. Powell sees weak global economic conditions as also pressuring the U.S. economy.

The other thing I would point to is the global dimensions. This is very much a global phenomenon and we’re seeing economic data from around the globe that is very, very negative and that too can weigh on U.S. economic performance over time.

In regards to economic conditions in foreign economies, there is little the Fed can do. In contrast to the U.S. with the government and Fed moving quickly with relief efforts, the reality is that most other countries cannot afford such measures. This means the crisis will be worse in other parts of the world and this has major implications for corporate earnings as a bearish trend.

Data suggests that an average company in the S&P 500 has over 40% of revenues coming from international markets. Some sectors like Technology and Consumer Staples are even more exposed to foreign countries. The International Monetary Fund, “IMF,” is forecasting a global recession of 3% this year and only a “partial recovery” in 2021. Even giving the recovery in the U.S. a benefit of the doubt, companies will still be challenged by weaker trends in international markets.

(source: FactSet)

The Next Move Is Lower

We believe that we are entering a new phase in the market cycle and the next major move is lower. There is too much complacency regarding the long-lasting economic implications separate from the public health crisis. While the initial sell-off in March included a level of panic and extreme market volatility based on the uncertainty regarding the pandemic, we think the market can now focus on cyclical headwinds and implications to valuation.

A real “V-shaped” recovery in the economy implies only transitory or temporary impacts that can be brushed aside for a quick rebound. If we accept that the underlying fundamental strengths of the U.S. and global economy have been materially damaged, the long-term growth trajectory of companies needs to be discounted. Equities should now be less valuable compared to where the market was at the beginning of the year.

The S&P 500 (SPY), NASDAQ 100 (QQQ), and the small-cap benchmark Russell 2000 (IWM) have each gained 29%, 27%, and 30% off their lows in March, respectively. Incredibly, over six months, QQQ is up 10%. SPY has seen only a moderate decline of 4% since November even as small caps have lagged.

The dynamic has been an outperformance among the mega-cap tech leaders like Amazon.com Inc. (NASDAQ:AMZN), Apple, Inc. (NASDAQ:AAPL), Microsoft, Inc. (NASDAQ:MSFT), Alphabet (NASDAQ:GOOG) (NASDAQ:GOOGL), and Facebook (NASDAQ:FB) which have large weightings in the major indexes. These five stocks together represent 22% of the S&P 500 and 48% of the NASDAQ 100 and are each up over the past six months with a significant 32% gain in AMZN and 25% by MSFT.

We bring this group up because we think the mega-cap market leaders can drive the market lower going forward. This group carries extreme market optimism and exuberance which have led to lofty valuations. At current levels, these stocks may already be pricing in a best-case scenario for the “medium-term”. Each of the big 5 stocks has at least a 20% downside in our view.

No company is immune to a recession. When you hear discussions regarding the recovery in 2021, it’s obvious that comparables and growth rates will appear amazing on a year-over-year basis considering the current low base. It will be more relevant to consider trends on a stacked two-year basis compared to 2019 which may have represented a “peak” for the economy and corporate operating measures. We expect measures like same-store sales and organic growth to be down in 2021 compared to 2019. Companies will struggle to reclaim the dynamic momentum observed in previous years.

We are particularly bearish on consumer staples which may have seen a temporary windfall from early-stage consumer buying trends during the pandemic. As a group, staples became a defensive trade, but we don’t see a reason for that momentum to continue. Companies like Walmart (NYSE:WMT), General Mills (NYSE:GIS), PepsiCo (NASDAQ:PEP) are trading near their all-time highs, but we expect to have a weaker outlook from here.

Watch the VIX

We’re looking at S&P 500 at 2,600 as a near-term downside target. Our message here is that the March low at 2,191 and 25% lower from the current level is still in play over the next year. The VIX peaked at a level of 85 in mid-March and has since declined to a more moderate 35 level which is still consistent with a high-risk environment.

Many investors may point to the currently declining VIX as evidence the worst is over and we can only rebound from here. We don’t believe that to be the case and highlight the financial crisis of 2008 and 2009 as an example where the market continued lower many months after the VIX peaked. Indeed, the VIX peaked at 89.5 on October 24, 2008, while the S&P would subsequently fall another 33% to its low on March 9th, 2009. On that day the VIX closed at 50.

The point here is that we expect renewed volatility, but that doesn’t mean we need to or will see more “13% limit down days” like what occurred in March. In our view, the next stage of this bear market will be based on a realization that the consensus “recovery” is not materializing as expected. The market will need to discount valuations to reflect the deeper structural cyclical pressures that are set to impact all sectors of the economy.

LINK: Seeking Alpha